How all-inclusive is the global banking system?

According to the latest edition of Global Findex, account holders are on the rise around the world, with 3 out of 4 of her adults worldwide now having a financial account.

Yet 1.4 billion adults remain unbanked.

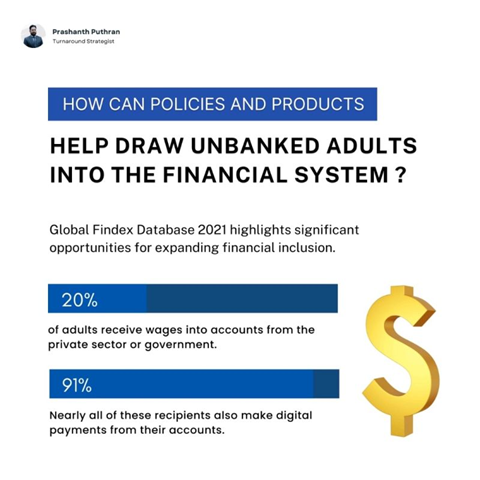

How can policies and products help draw unbanked adults into the financial system?

Global Findex Database 2021 on how account holders use their accounts to pay, save and borrow, and how these financial services interact as part of the broader financial ecosystem.

The findings highlight significant opportunities for expanding financial inclusion.

So one of the financial transactions unbanked adults are already doing is making payments.

Payments to your account act as a gateway to use other financial services.

According to Global Findex 2021 data, in developing countries, 20% of adults receive wages into accounts from the private sector or government (Figure 1).

Nearly all of these recipients (91%) also make digital payments from their accounts.

Digitizing cash payments is a proven way to increase account ownership.

Millions of unbanked adults still receive gradual cash payments from employers and governments.

Global Findex data suggests that alternating some of these payments to accounts could increase financial inclusion and access to financial services among her 1.4 billion unbanked adults.

Suggests that there is Digitizing such disbursement is a proven way to develop account ownership.

By creating an environment where wage payments can be used for greater financial inclusion, she can reduce the number of unbanked adults by 165 million.

Global Findex 2021 data shows that 165 million unbanked adults receive cash-only wage payments from the private sector (Map 1).

The cash-to-account migration of wage payments and other types of payments (such as payments for the sale of agricultural products) can serve as an entry point into the formal financial system.

The challenge for affairs and governments is to arrange that digital remuneration is safer, more affordable, and more transparent than cash-based alternatives.

This allows employees to use their accounts to brush up on their financial well-being.

#fintech #financeleadership #africanbusiness #growthanddevelopment #leadershipdevelopment